In the digital age, it is no surprise that people are preferring to use online banks over traditional community banks. Consumers are often drawn to community driven institutions because they want a financial partner that represents their values, invests in their communities and that supports businesses they care about.

The COVID-19 lockdowns revealed a deeper vulnerability for these institutions as patrons were no longer going into brick and mortar locations. This made the interpersonal relationships that the community banks rely on for growth almost impossible. The value proposition of institutions should be projected into the digital realm.

According to a recent survey clients drastically favored using online banking apps because of their accessibility and the different tools these apps provide to assist with wealth management. Tools such as early wage access, financial wellness, online payments, budget and spending guides. Moreover, people between the ages of 25-34 are more likely to use an online bank, with those 35-44 also preferring this form of banking.

With these statistics in mind, what can community banks do to remain relevant?

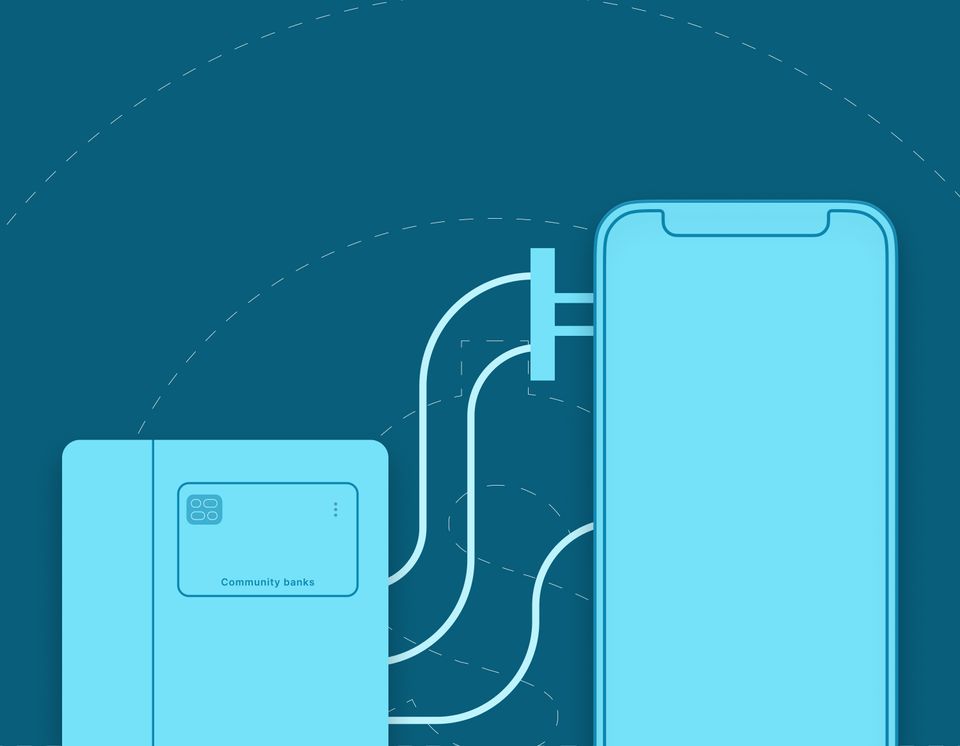

One suggestion is partnering with financial institutions that recognize not only your institutions values but also that serving smaller or even more distinct communities (such as pig farmers, babysitters, builders, etc...) could be beneficial in promoting not only economic growth but financial wellness and prosperity within those communities. In order to maintain relevance, community banks must make the leap into the digital era. Why are community banks hesitant to make the digital leap?

Community banks may prefer a more traditional approach to banking because it is familiar. These institutions are often reluctant to upgrade due to possible fears of data loss or migrating from their legacy core providers or they might recognize the need but may prefer to wait for the right time. However, this might not be the best strategy in the long run given how rapidly consumer expectations are changing and the lag in the institution's ability to catch up.

The good news is there are solutions for these institutions and it’s important for them to get started as soon as possible by working with financial technology partners that can drive innovation from outside the core, companies like Kasasa, Deposits.inc or Synctera all have a great track record of spurring growth and innovation for FIs without a big technical burden.